If you’ve been thinking about buying a home, mortgage rates are probably top of mind for you. They may even be why you’ve put your plans on hold for now. When rates climbed near 8% last year, some buyers found the numbers just didn’t make sense for their budget anymore. That may be the case for you too.

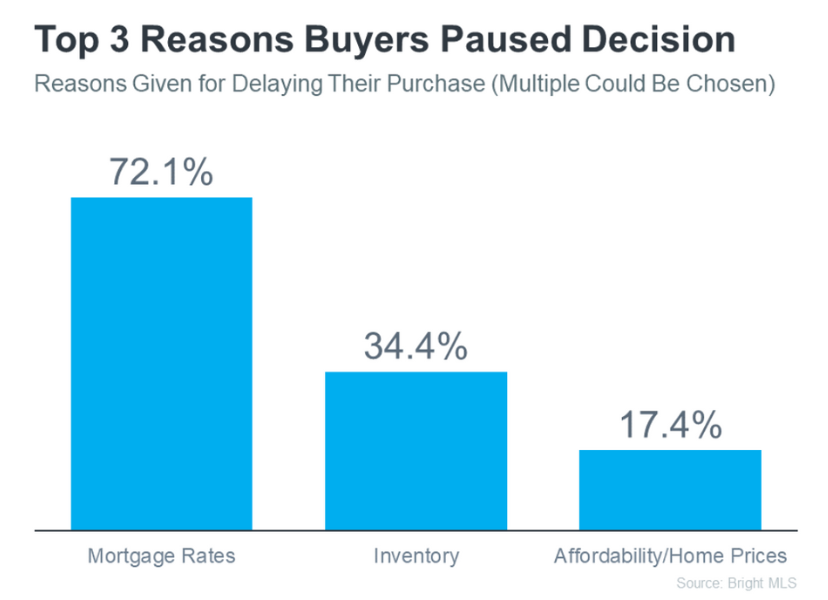

Data from Bright MLS shows the top reason buyers delayed their plans to move is due to high mortgage rates (see graph below):

Mortgage rates have come down off their peak last October. And while there’s still day-to-day volatility in rates, the longer-term projections show rates should continue to drop this year, as long as inflation gets under control. Experts even say we could see rates below 6% by the end of 2024. And that threshold would be a gamechanger for a lot of buyers. As a recent article from Realtor.com says:

“Buying a home is still desired and sought after, but many people are looking for mortgage rates to come down in order to achieve it. Four out of 10 Americans looking to buy a home in the next 12 months would consider it possible if rates drop below 6%.”

While mortgage rates are nearly impossible to forecast, the optimism from the experts should give you insight into what’s ahead. If your plans were delayed, there’s light at the end of the tunnel again. That means it may be time to start thinking about your move. The best question you can ask yourself right now, is this:

What number do I want to see rates hit before I’m ready to move?

The exact percentage where you feel comfortable kicking off your search again is personal. Maybe it’s 6.5%. Maybe it’s 6.25%. Or maybe it’s once they drop below 6%.

If you’ve put your plans to move on hold because of where mortgage rates are, think about the number you want to see rates hit that would make you ready to re-enter the market.

Once you have that number in mind, contact us at Butler Mortgage so you have someone on your side to let you know when we get there.